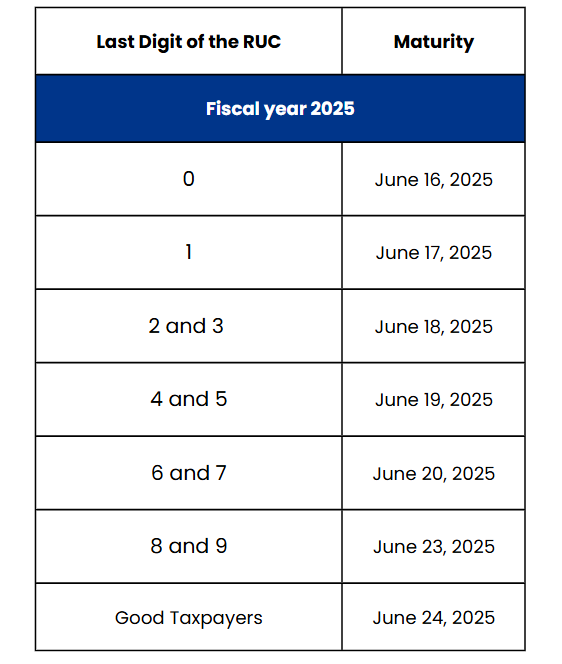

The deadline for submitting the Informative Affidavit for the Local Transfer Pricing Report for fiscal year 2024 is June 16-24, 2025 , as shown in the following schedule.

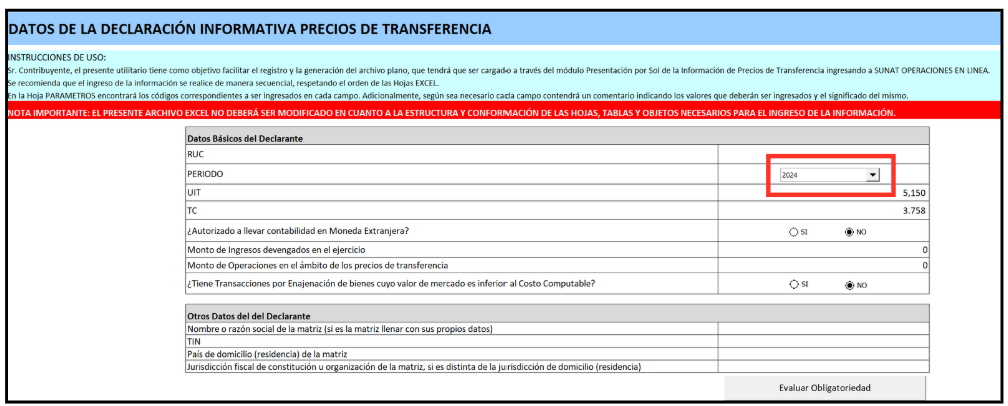

It should be noted that, unlike other years, since March 2025, the electronic box for the 2024 Local Report Utility (Annex 2) has been enabled, as shown below.

At TP Consulting, we have been warning about the increase in SUNAT ‘s transfer pricing audits, especially in the following key areas:

- Benefit Test: SUNAT has begun sending notices for alleged noncompliance with this obligation. See Alert No. 008-2024-PE, where we warn about notifications related to inconsistencies detected in the Transfer Pricing adjustment, resulting from the cross-referencing of the Local Report and the Income Tax Return, for fiscal years 2019 and later.

- Cross-referencing of information between the Local Report and the Income Tax Return: Both formal and substantial inconsistencies have been identified. In Alert No. 004-2024-PE, we reported that SUNAT has begun sending out notification letters for non-compliance with the Benefit Test (2019–2022 fiscal years), in addition to inductive letters linked to the 2023 Local Report and notifications related to the Master Report for fiscal years 2019–2022.

These topics have been covered in depth in our technical webinars. If you’d like to access the recordings, please request them by emailing [email protected].

| DATE | WEBINAR | THEME |

| 27/02/2025 | Benefit Test: Mandatory documentation for deducting costs and expenses in Intragroup Services | ▪️Current regulations for deducting costs and expenses for intragroup services in the LIR (Taxpayer Registry). ▪️Practical examples of redistribution of costs and expenses. ▪️Inconsistencies detected by SUNAT in 2024. |

| 04/12/2024 | Sixth Transfer Pricing Method: Opportunity to rectify export and import declarations of commodities before the end of 2024 | ▪️Modifications to the Commodity Export and Import Declaration submitted to SUNAT in October 2024. ▪️Incorporation of the Sixth Method analysis into the Local Transfer Pricing Report in June 2024. ▪️Characteristics of the technical, economic, and financial study related to Commodities: Sixth Method in Peru: Theory and Reality. |

| 12/11/2024 | Inconsistencies detected by SUNAT regarding the Benefit Test, Local Report, and Master Transfer Pricing Report obligations | ▪️Transfer Pricing Obligations and the situation in Peru as of November 2024. ▪️What should the Benefit Test include and how does it relate to Transfer Pricing Reports? ▪️Main errors committed by companies in Peru. ▪️Fines, corresponding reductions, statute of limitations, and interruption of the statute of limitations. |

| 19/09/2024 | New SUNAT Commodity Declaration Format for the Local Transfer Pricing Report: Due June 18, 2024 | ▪️Sixth method applicable to Peru in the case of commodities. ▪️What has been happening in reality? ▪️Scope of SUNAT Superintendency Resolution No. 000123-2024/SUNAT published on June 14, 2024 |

| 25/04/2024 | Benefit Test: Mandatory documentation for deducting costs and expenses in intragroup services | ▪️Current regulations for the deduction of costs and expenses related to intra-group services under the Income Tax Law. ▪️Practical examples of cost and expense allocation. ▪️Audits and international cases related to the Benefit Test: documentation requested by the Tax Administration. ▪️Outlook for the 2023 Transfer Pricing Return. |